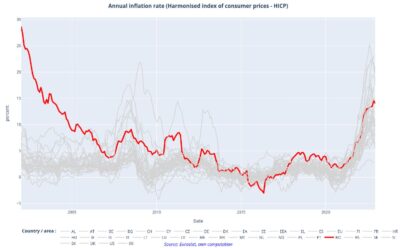

An analysis of the evolution of inflation in Romania over the last 20 years highlights numerous medium-term cycles, influenced by local and international conjunctures often very different specific to the respective moments. We can say that there is a point that separates the evolution trends at the local level in relation to the European ones, this being around the year of Romania’s accession to the European Union. The graph below shows this evolution for Romania and the economies of the European Economic Area using harmonized indices of consumer prices calculated and published by Eurostat (inflation dynamics in the United States of America are added to complete the overall picture).

Beyond all the particularities of each year, the graph below shows a very important structural change that makes the current situation fundamentally different from the economic and financial context of Romania at the beginning of the period analyzed. This difference is so contrasting that it can be noticed by anyone who looks closely at the graph, without requiring specialized knowledge. Before the accession to the European Union, for the period 2002-2007, it can be observed that the level and dynamics of inflation in Romania were substantially different from the trends of the moment at the European and global level. For the same time interval, however, a consistent process of convergence towards the general level and the overall direction of inflation in the European economic space is also observed. In my opinion, this illustrates, once more, the major decoupling that existed in the past between the Romanian economy and the European one, but also the important transformation it went through during that period, as well as the effort of the central bank superimposed on the preparation and the operationalization of inflation targeting regime.

Before the accession to the European Union, for the period 2002-2007, it can be observed that the level and dynamics of inflation in Romania were substantially different from the trends of the moment at the European and global level. For the same time interval, however, a consistent process of convergence towards the general level and the overall direction of inflation in the European economic space is also observed. In my opinion, this illustrates, once more, the major decoupling that existed in the past between the Romanian economy and the European one, but also the important transformation it went through during that period, as well as the effort of the central bank superimposed on the preparation and the operationalization of inflation targeting regime.

We can also see on the graph that after 2007, when inflation in Romania significantly reduced the major gap against the level observed in most other European economies, there followed a period of approximately 5 years, until 2012, in which, although the dynamics of inflation at local level was much more synchronized with the developments in the wider European area, however the level remained mostly higher in comparative terms. Returning to the previous parallel, I believe this correlation in dynamics is in turn an expression of the fact that the degree of integration of the Romanian economy had already become high enough for price trends at local level to be more significantly correlated with those at the European level.

Later, in the second half of the period analyzed and presented in the graph, this correlation remained significant, broadly speaking, with ups and downs. So, we see that in the last 10 years (between 2012 and 2022) inflation trends in Romania were in most situations synchronized with those at the European level, even if there were also periods when local inflation was at the top or on the contrary, at the bottom of the European platoon. With Romania’s accession to the European Union, not only did the economy become more strongly anchored to the European economy, by strengthening trade ties with member countries, but also the legal, institutional, and economic policy framework became significantly more synchronized with the European one. This is also true from the perspective of the central bank, whose efforts to combat inflation could not (for a variety of reasons related to economic rationality) abstract from the actions and monetary policy decisions of the relevant central banks in the neighborhood or those of the European Central Bank. For example, the substantiation Report of the National Plan for the Adoption of the Euro published in December 2018 noted that in 2017 the convergence of prices in Romania was about 52.2% compared to their level in the European Union.

As is natural, after this moment placed around 2012, which I consider as one of the relevant turning points of the last 20 years, influences of the structural particularities of the local economy continued to be visible in the evolution of inflation in Romania, but against the background of a much more visible overall synchronization with the European trends. The responses of the inflation rate to the various shocks continued to be influenced by the structural characteristics of the economy, reflected also in the composition of the consumption basket. Today as well as more than 5 years ago, the CPI basket in Romania allocates a weight of over 30% to food products (among the highest at European level). At the same time, a significant part of the processed food consumed in Romania comes from imports. In this context, the same report that I referred to above noted as early as 2018 that the evolution of the annual inflation rate is significantly influenced by elements outside the scope of monetary policy, by the nature of domestic or international supply shocks and administrative decisions, as well as fiscal measures.

Such an episode is represented by the period of accentuated disinflation from 2014-2016, when the annual inflation rate in Romania showed, against the background of successive reductions in indirect tax rates, a pronounced downward trend, consistent with the predominantly downward evolution of base inflation. At the time, the decline in raw material prices (especially energy), as well as the very good agricultural year, contributed to this trend. In addition, HICP dynamics then reflected, through the evolution of the prices of imported goods, persistently low inflation in the euro area.

Interestingly, after more than 5-6 years, broadly many of these factors became relevant again in 2022, just not in the same direction. We therefore recorded major effects on inflation at the local level as a result of changes in the prices of raw materials, energy, fuels, imported processed foods, volatile prices of agricultural products and the effects of administrative decisions and support programs. Some of these had contributions to the increase of inflation, others to its decrease in relation to the much higher potential level, but on the whole they all remained relevant, being still outside the effective influence of monetary policy instruments.

Returning to our chart, we see a possible reversal of the inflation trend at the end of last year, which would equate to a reduction in the pace of price growth. This potential trend is visible at the European level and is supported by the recent price reductions observed in the trading markets of fuels, energy, other important raw materials for industry, the reduction in demand as a result of the tightening of monetary conditions and the decrease in purchasing power, the moderation of anticipations etc. Romania still fits within this platoon, it is neither at the highest level nor at the lowest. The recent reduction in the inflation rate in Romania in December suggests that again, at the moment, the price dynamics at the local level will not make an exception from the general trends manifested at the European level.

All of the above I believe argues that, already for many years now, the degree of economic, financial, institutional, and policy integration of Romania within Europe is significant enough so that the external factors that influence price dynamics are common, external demand and prices have an important impact on domestic prices, and the economic policy response is sufficiently harmonized not to lead to major long-term discrepancies.

In the specialized literature, it is argued that in emerging economies in the process of convergence towards a more developed economic area, as is the case of Romania as a member state of the European Union, the dynamics of prices is somewhat wider compared to the average of the group of states in which it aims to integrate (for structural reasons fueled by the convergence process itself, including as an effect of the convergence of purchasing power, living standards, and quality of life). The International Monetary Fund predicted at the end of last year that global inflation would decrease, but in the case of emerging economies the decrease could be somewhat more modest. From this perspective, I think it is reasonable to expect to see in the future, in the medium term, episodes where the level of inflation places us in the upper half of the European country group, but I think it is very unlikely to see a consistent period during which we would be on a divergent trend from it.

The mathematics of inflation is not at all simple, but beyond that it is worrying that relatively close values of inflation in various countries are perceived differently by the population. Inflation can be interpreted as a regressive indirect tax because it mainly affects those with low incomes. In fact, this is precisely what must stimulate the operationalization of programs for increasing the degree of economic convergence of emerging countries, so that their population feels the effects of inflation in a mitigated way due to the higher degree of development.

: Inflation in Romania in the European context – milestones of the last 20 years")

COMMENTS